Stocks to Buy Now from Dan Loeb's Third Point - SentinelOne Stock analysis vs CrowdStrike (CRWD)

While CRWD is spending >3x in opex but generating almost 6x in ARR, SentinelOne is growing at double the rate.

Dan Loeb's Third Point is a major holder in SentinelOne, accounting for >9% of his portfolio and first owned back in Q2 2021. The only larger shareholder is Insight Venture Partners.

On the other hand, CrowdStrike is a much more institutionalized stock with key shareholders such as BlackRock, Vanguard, Tiger and Allianz.

We calculated figures in this note using SentinelOne's Q4 2022 Shareholder Letter and CRWD's Investor Presentation.

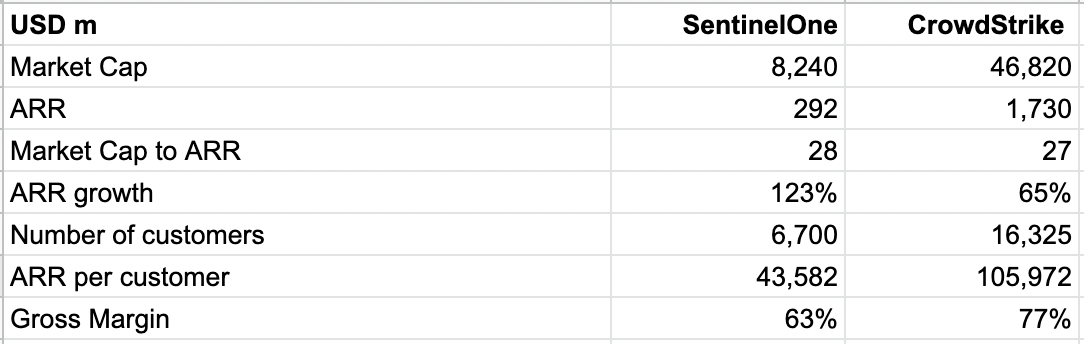

CRWD is almost 6x larger than SentinelOne in terms of both market cap and ARR, implying they are both trading at around 27-28x ARR multiples.

SentinelOne is growing at double the rate of CRWD but CRWD's ARR per customer is double that of SentinelOne and also has higher gross margin.

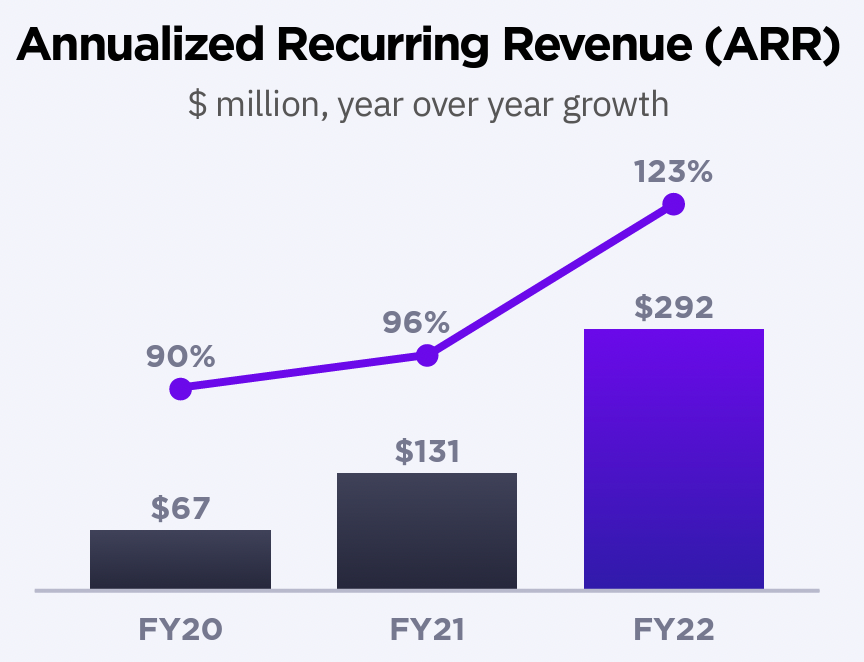

Specifically, SentinelOne's ARR is growing at a growing rate, which is always a positive.

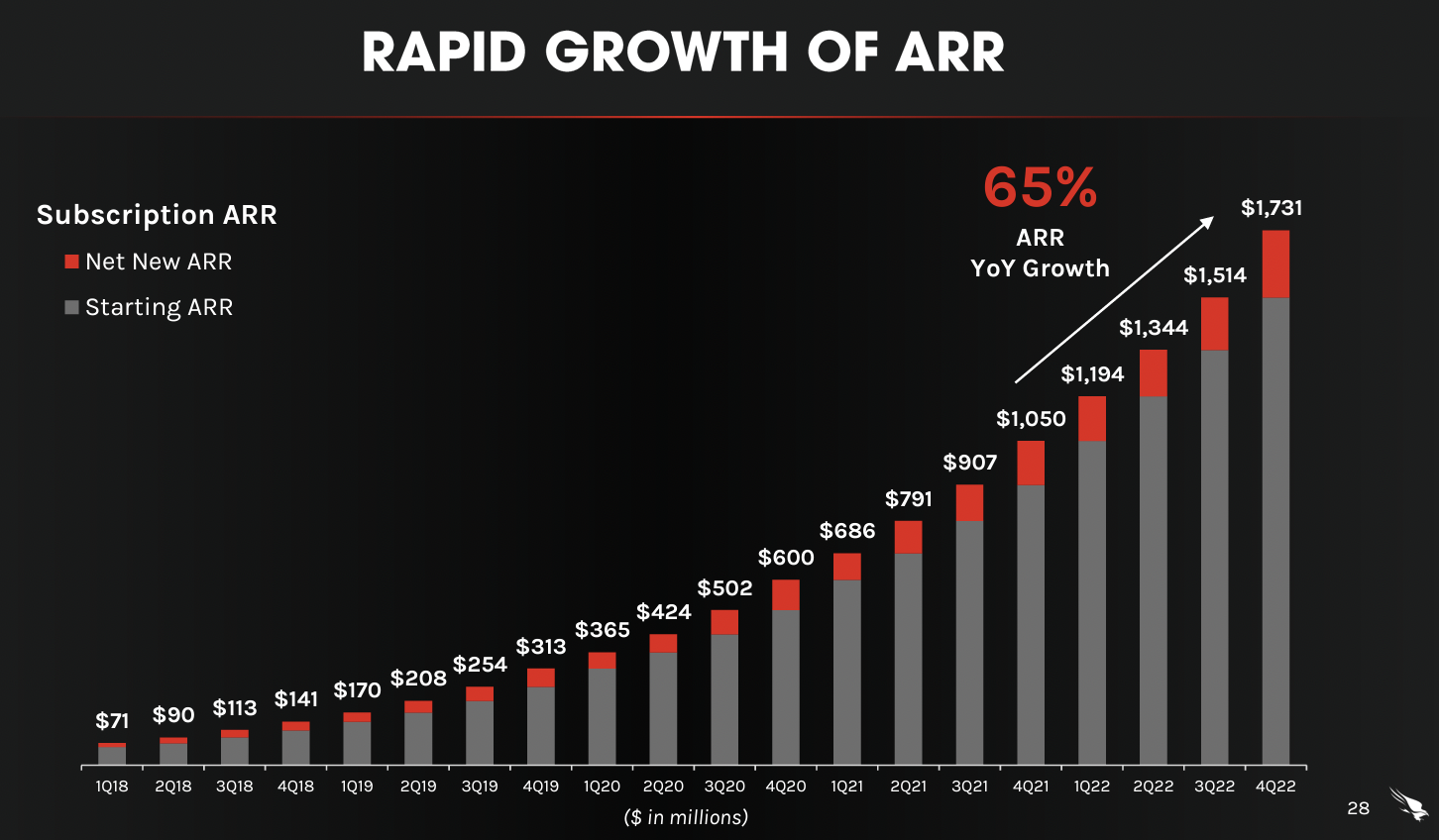

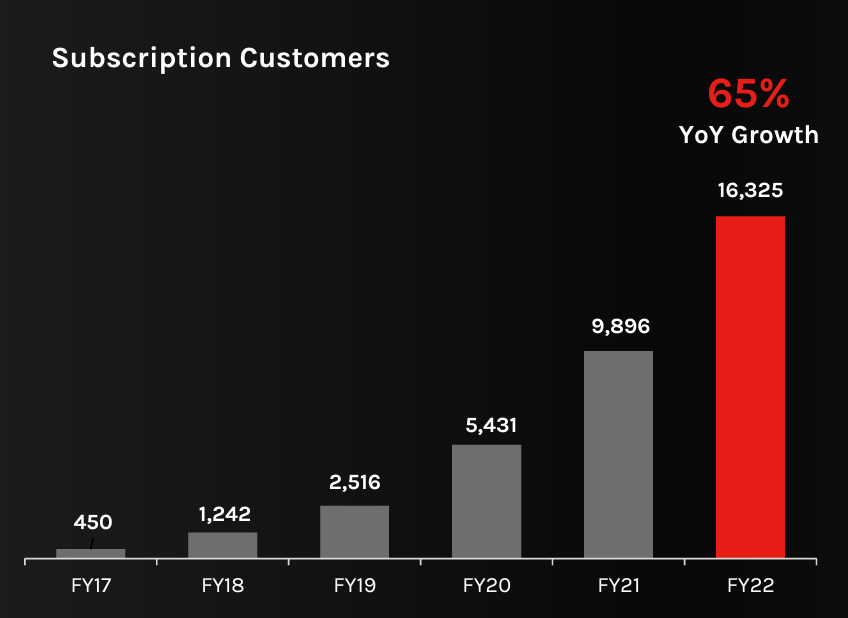

Similar to SentinelOne, CRWD's ARR is pretty much doubling every year in the past few years so the latest 65% is actually a slowdown.

Specifically, ARR growth is driven by CRWD's customer count basically doubling every year since FY17.

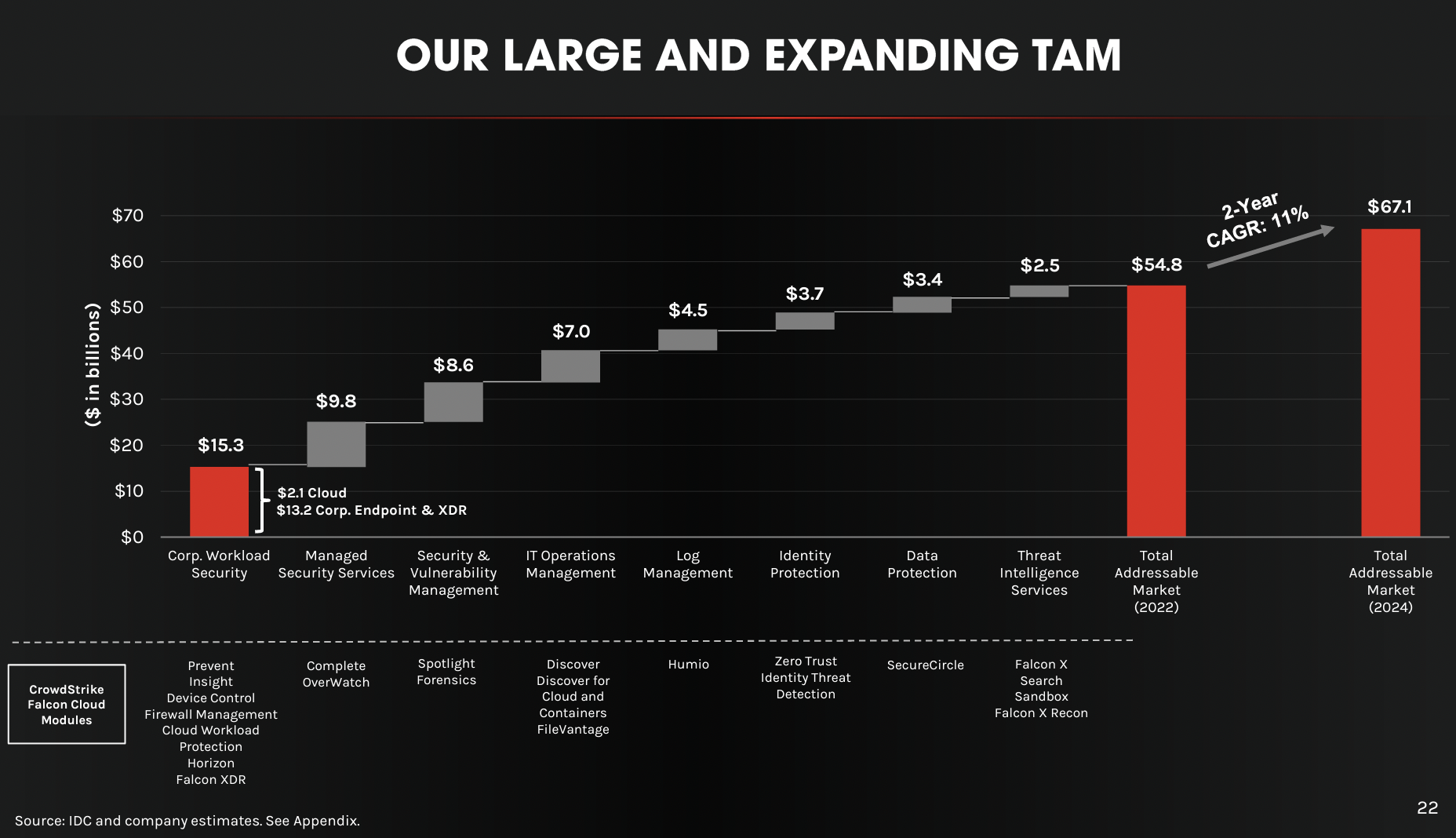

Generally, high growth tech businesses are difficult to value using traditional financial metrics.

While one can always look at ARR, growth, gross margin, net retention etc, perhaps more importantly, expanding the Total Addressable Market (TAM) is a more strategic, long term and sustainable way to boost valuation.

Ceteris paribus, a business with an ever expanding TAM should be worth more.

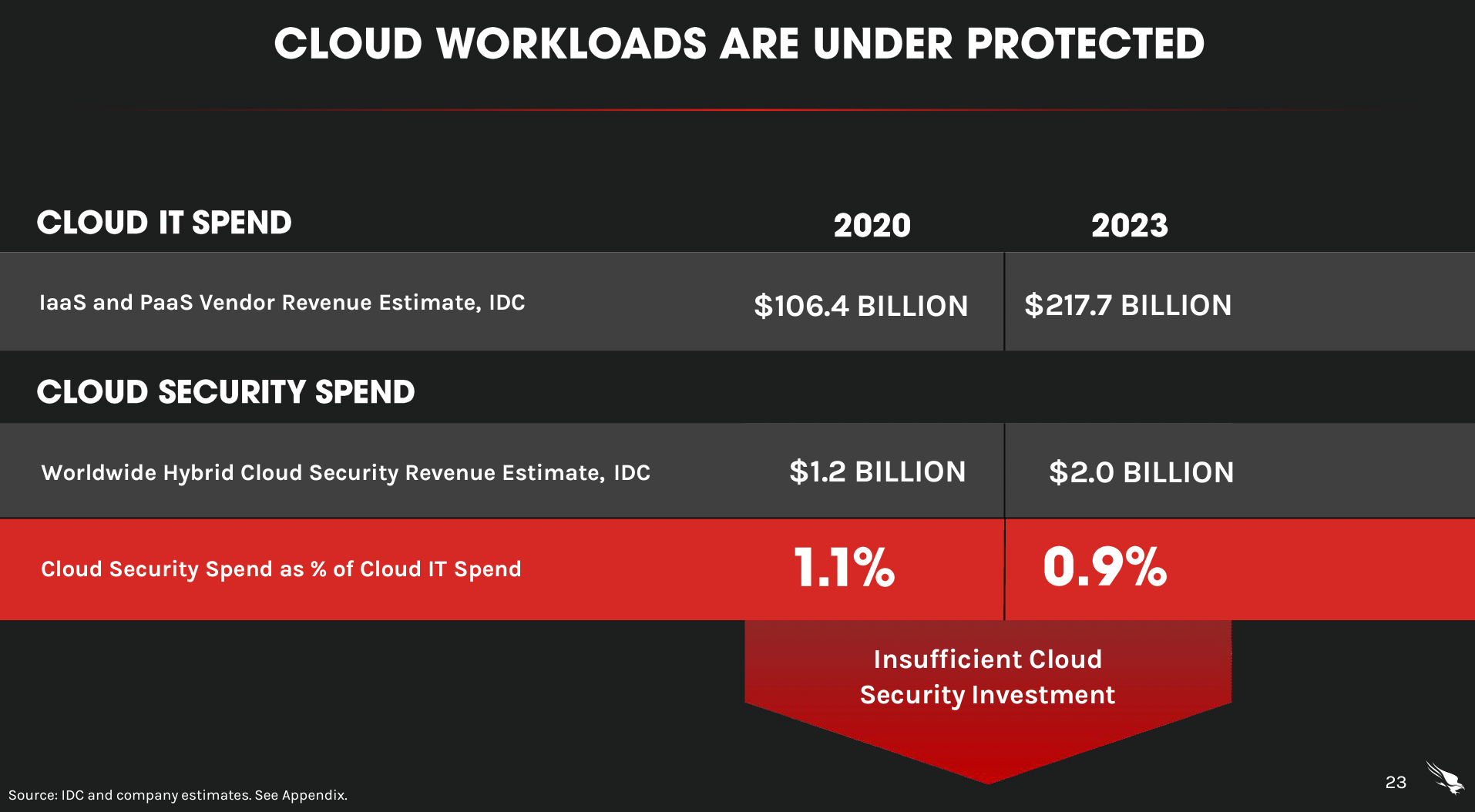

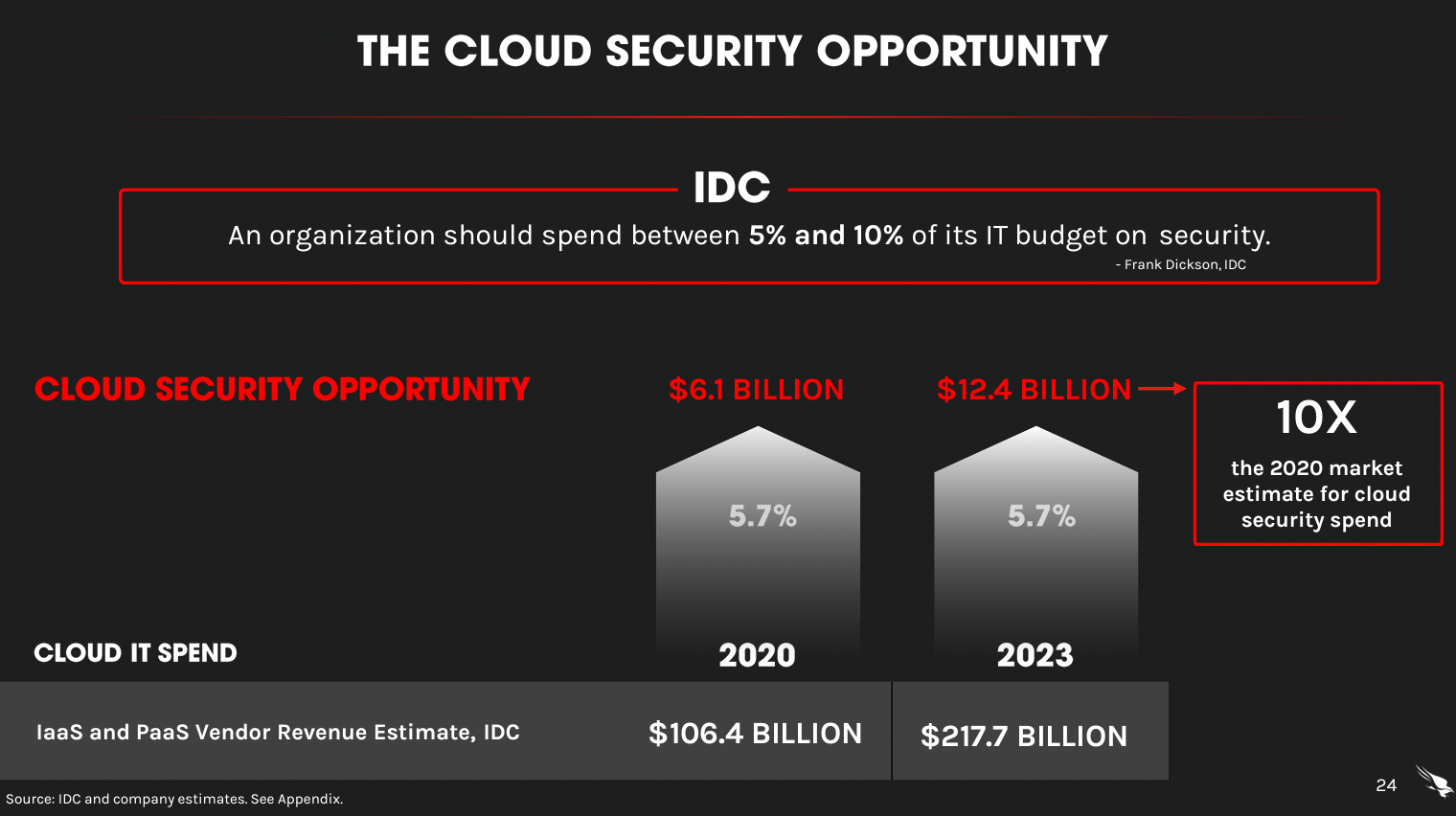

According to CRWD and IDC, cloud security spend is underinvested...

...hence opportunities.

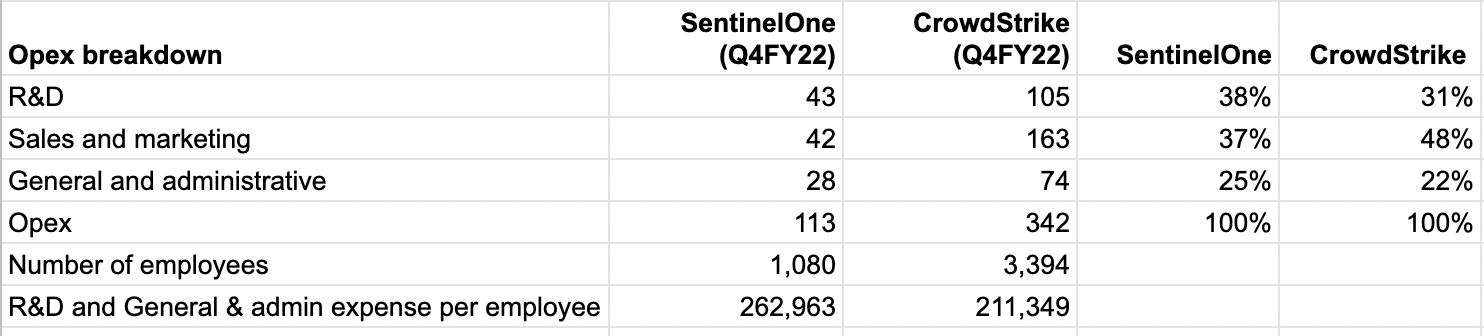

In terms of operating expenses (opex) breakdown, SentinelOne spends more on R&D while CRWD spends more on sales and marketing.

It also appears that average compensation per employee for SentinelOne is slightly higher than CRWD.

Recall CRWD is almost 6x the size of SentinelOne, this is not reflected in the absolute amount of opex. Specifically, CRWD only spends more than 2x in R&D, >3x in sales and marketing and >2x in general and admin. In other words, CRWD is spending >3x in opex but generating almost 6x in ARR.

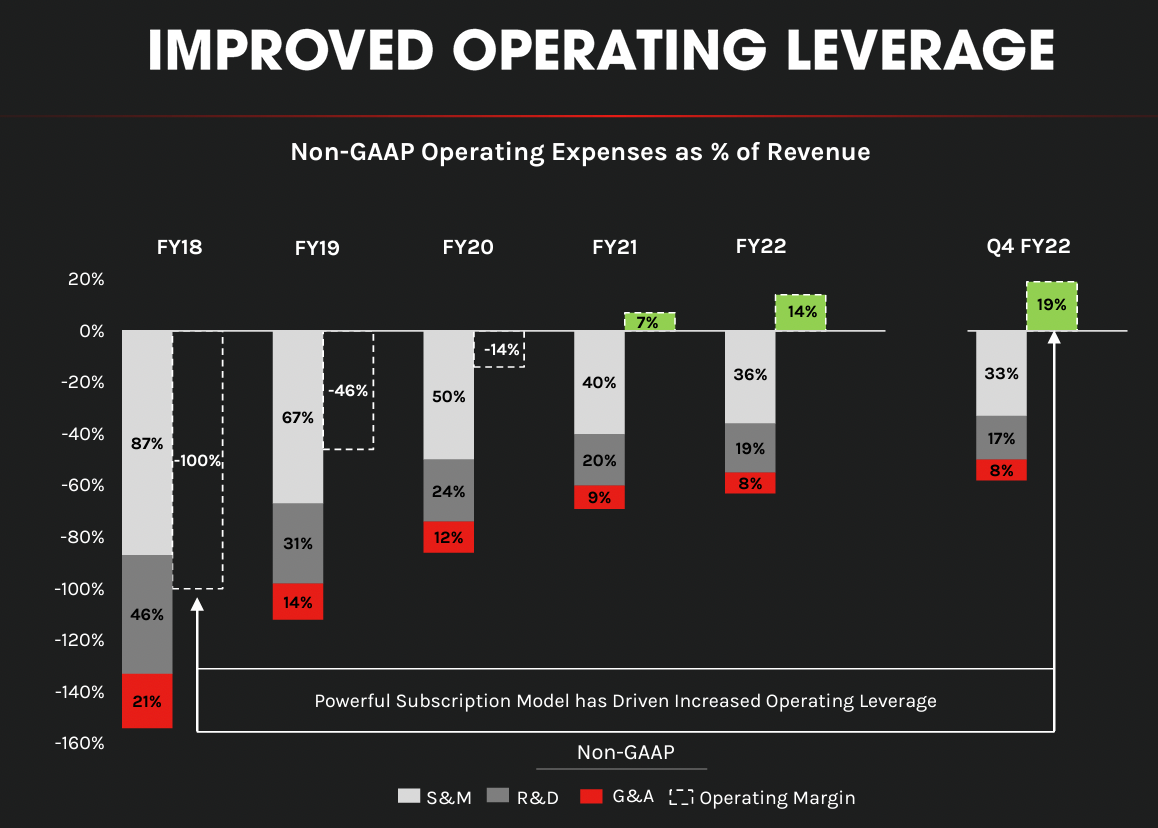

Specifically, CRWD has been improving its operating leverage in the last few years and has been reporting a positive operating margin since FY21.

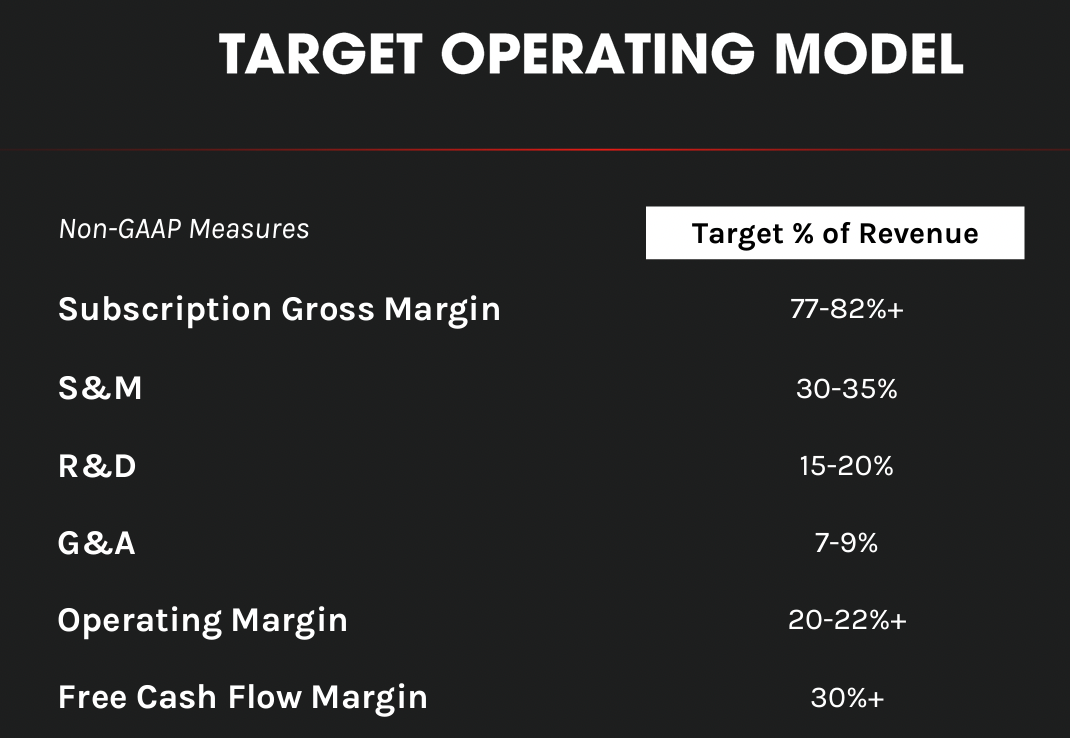

At 19% in Q4 FY22, operating margin is already close to CRWD's target level of 20-22%+. Also, notice that CRWD's target S&M spend is more than R&D.