Fintech Stocks to Buy Now - Upstart (UPST stock) analysis (November 2021 Update)

(November 2021 Update) Upstart takes on risks that would have been otherwise rejected by traditional lenders and lower interest rates for these risks.

As per Upstart's 2020 Annual Report, "our AI model approves 27% more borrowers than high-quality traditional lending models with a 16% lower average APR for approved loans."

That is, Upstart's key edge is taking on risks that would have been otherwise rejected by traditional lenders and lower interest rates for these risks. In other words, Upstart brings out the true underlying risks through its big data approach.

Market Cap

Upstart's market cap is driven by the Market Share (A) of its Target Market (B) by Profit Margin (C).

Specifically, for Personal loan originations,

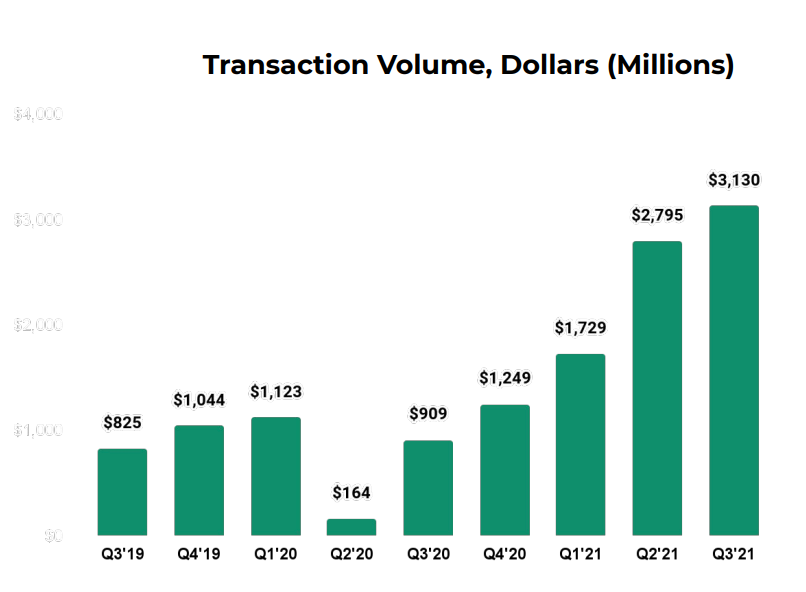

(A) is ~13%. According to Upstart's Q3 2021 Earnings Presentation, Upstart has Transaction Volume totalling $7,654m in the three quarters to Q3'21.

Assuming Upstart will do another $3b or so in volume in Q4'21 and the yearly personal loans origination at $81b, this would imply Upstart's market share is around 13%.

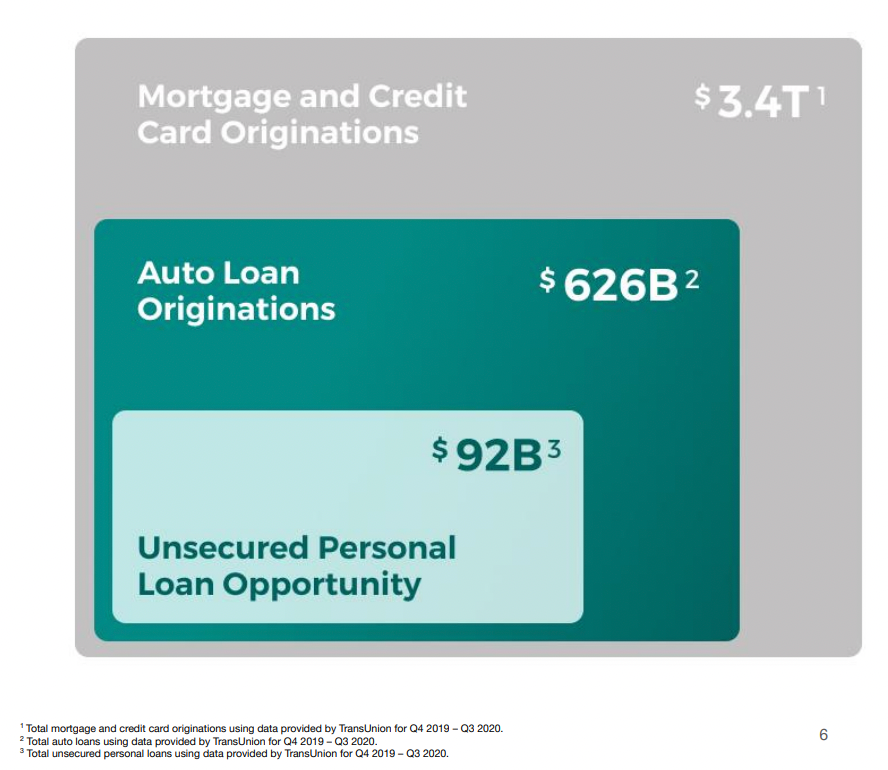

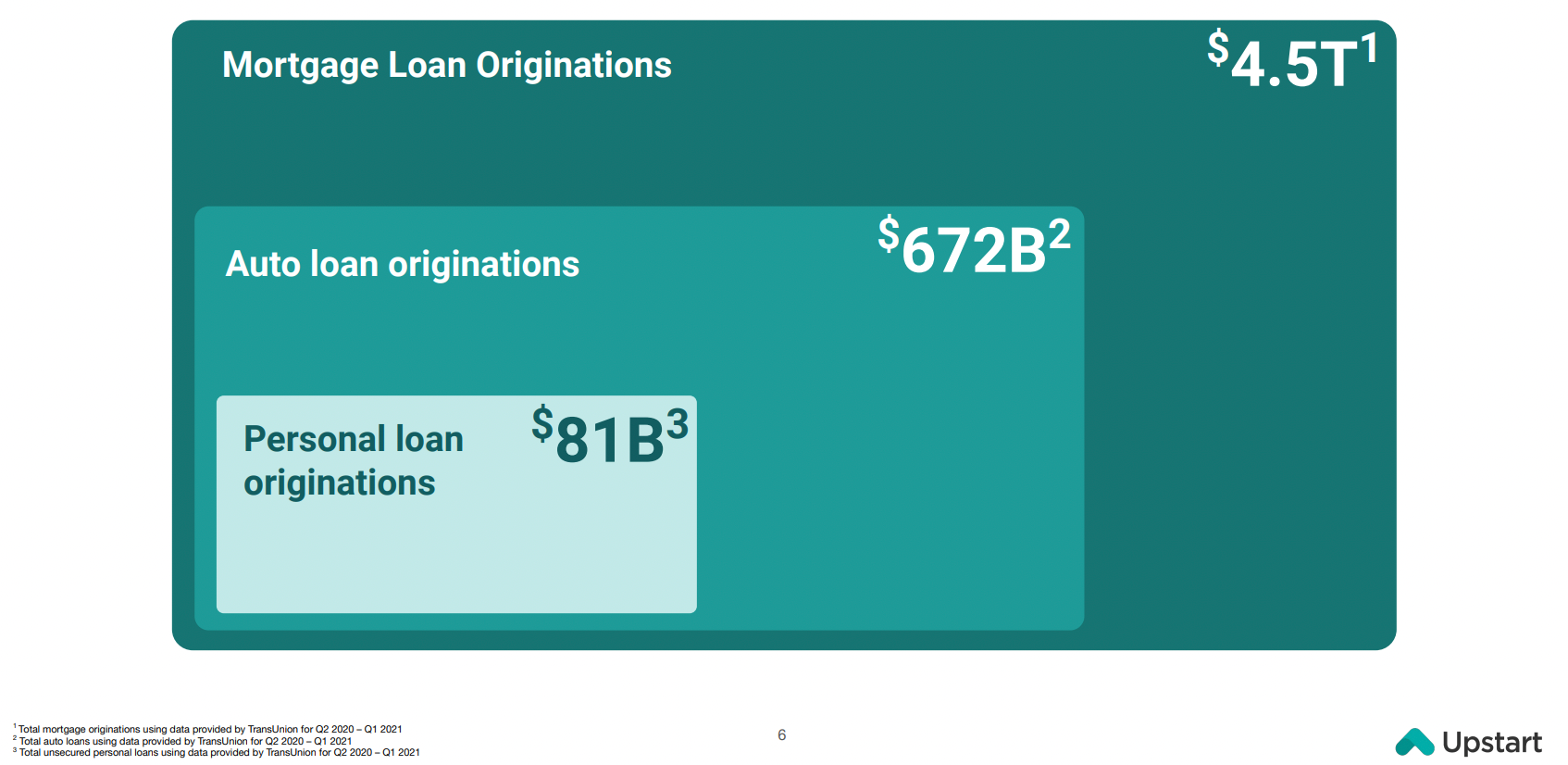

(B) is $81b as per Upstart's Q3'21 Earnings Presentation and data provided by TransUnion for Q2 2020 – Q1 2021.

This figure has shrink by 12% from Q419 to Q121 as per below.

Q4 2019 – Q3 2020 (Upstart Q1 2021 Earnings published on May 11, 2021)

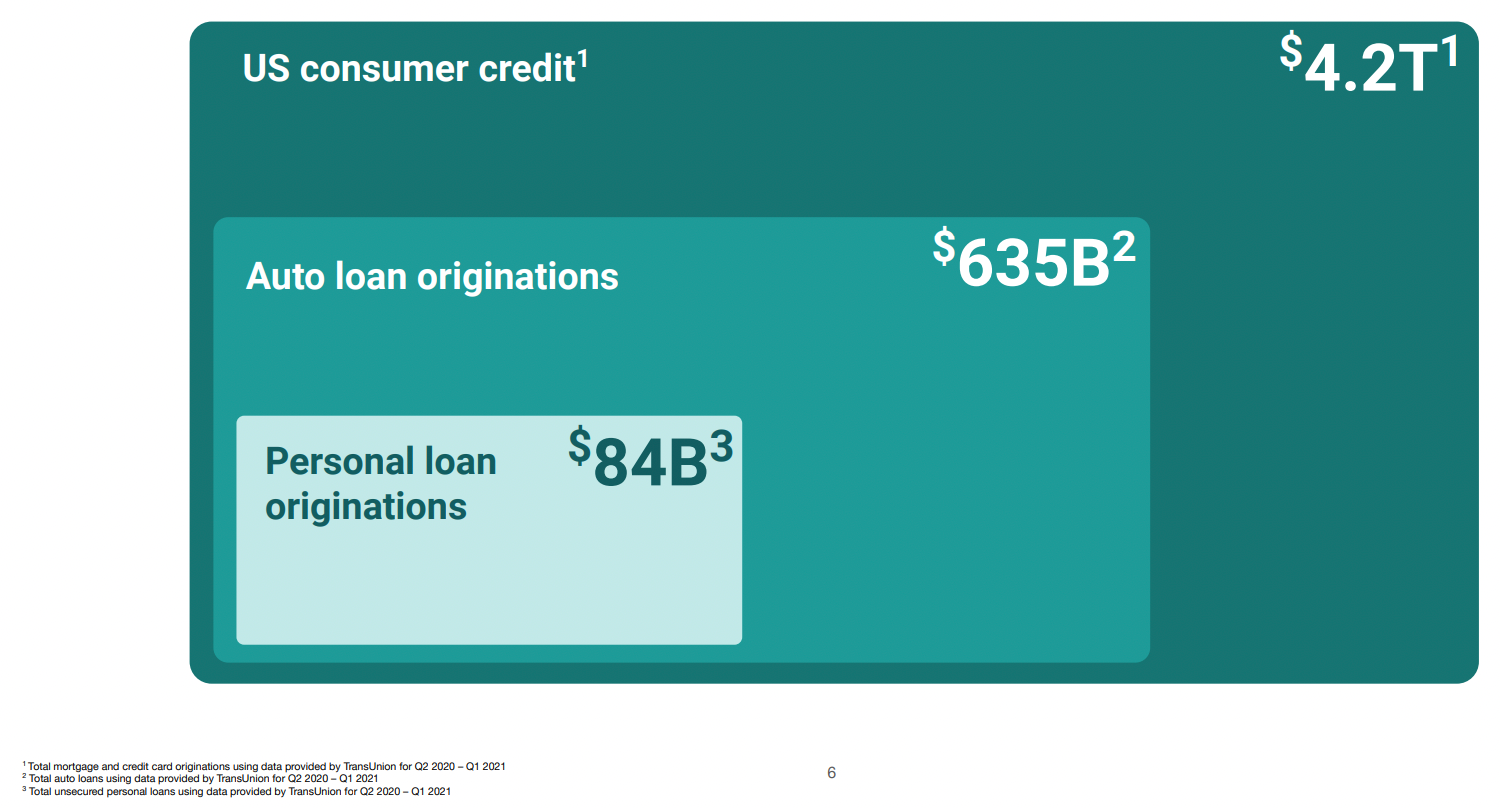

Q2 2020 – Q1 2021 (Upstart Q2 2021 Earnings published on August 10, 2021)

Q2 2020 – Q1 2021 (Upstart Q3 2021 Earnings published on November 9, 2021)

As per above, Upstart also defines a larger Target Market though there are some inconsistencies in how it is presented.

In the Q1'21 Earnings Presentation, it is defined as Mortgage and Credit Card Originations ($3.4t).

In the Q2'21 Earnings Presentation, it is changed to US consumer credit (but has increased to $4.2t), which is still defined as Mortgage and Credit Card Originations.

In the Q3'21 Earnings Presentation, it became just Mortgage Loan Originations but has further increased to $4.5t or by 32% from Q4'19 to Q1'21.

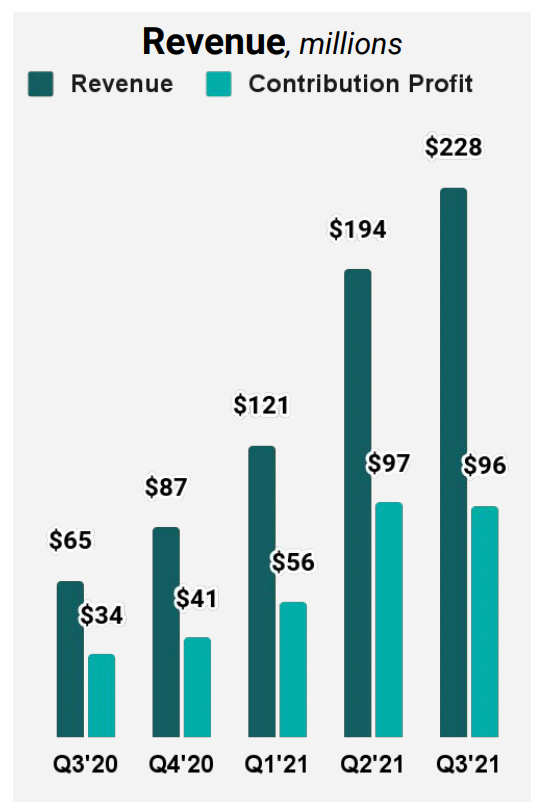

(C) is Upstart's Contribution Profit by Transaction Volume, Dollars. If using Q3'21's numbers, Contribution Profit is $96m and Transaction Volume is $3,130m. This implies ~3% margin or Upstart making 3% on the loan balance.

The spreadsheet on Upstart's Market Cap is available in our members' section. Email [email protected] for details.

Regulatory Risk

As per the extract below from Upstart's Q3'21 10-Q, it is subject to monitoring from the CFPB.

after significant collaboration with the Consumer Financial Protection Bureau, or CFPB, the CFPB issued Upstart the first no-action letter in 2017 and, upon its expiration, we received a second no-action letter regarding the use of our Al model to underwrite and price unsecured closed-end loans. The current no-action letter expires on November 30, 2023

For example, in February 2020, we received a letter from five members of the U.S. Senate asking questions in connection with claims of discriminatory lending made by an advocacy group. We responded to this inquiry, and in July 2020, three of the Senators issued their findings from this inquiry, writing a letter to the Director of the CFPB recommending the CFPB further review Upstart’s use of educational variables in its model and requesting that the CFPB stop issuing no-action letters related to the Equal Credit Opportunity Act, or ECOA. Further, the recently appointed CFPB Director indicated in remarks in October 2021 that safeguarding against algorithmic bias is a priority for the CFPB under the new leadership. We have been subject to other governmental inquiries on this topic including an inquiry in June 2020 from the North Carolina Department of Justice.

Credit Karma

As per the extract below from Upstart's Q3'21 10-Q, Credit Karma is a key originator for Upstart's business.

A significant number of consumers that apply for a loan on Upstart.com learn about and access Upstart.com through the website of a loan aggregator, typically with a hyperlink from such loan aggregator’s website to a landing page on our website. For example, the nine months ended September 30, 2020 and 2021, 52% and 44%, respectively, of loan originations were derived from traffic from Credit Karma. Our most recent agreement with Credit Karma dated November 6, 2020 provides that either party may terminate our arrangement immediately upon a material breach of any provision of the agreement or at any time, with or without cause, by providing no less than 30 days’ notice. Even during the term of our agreement, our agreement does not require Credit Karma to display offers from lenders on Upstart.com nor prohibit them from working with our competitors or from offering competing services.

While we are planning to move towards more direct acquisition channels, we anticipate that we will continue to depend in significant part on relationships with loan aggregators to maintain and grow our business.

Data on the direct acquisition channels contribution is in the extract from the 2020 Annual Report below,

The percentage of loan originations that were derived from traffic from Credit Karma was 38%, 38% and 52% in 2018, 2019 and 2020, respectively, and the percentage of loan originations that were derived from direct mail was 28%, 23% and 12%, in 2018, 2019 and 2020, respectively. No other marketing channel contributed significantly compared to Credit Karma and direct mail.

There is further explanation on how Credit Karma had a program that affected the number of loan applicants directed to Upstart.

In this regard in 2020, Credit Karma began directing more customer traffic to a program that hosts and aggregates the credit models of other loan providers directly on its platform for the purpose of giving credit offers. In late 2020, we experienced a reduction in the number of loan applicants directed to the Upstart platform by Credit Karma and a corresponding decrease in the number of loans originated on our platform because we had limited participation in this program. If traffic from Credit Karma decreases again in the future as a result of this program or for other reasons, our loan originations and results of operations would be adversely affected. There is also no assurance that Credit Karma will continue its contract with us on commercially reasonable terms or at all. Further, on December 3, 2020, Credit Karma was acquired by Intuit Inc. It is possible Intuit may not continue our agreement on commercially reasonable terms or at all, which would adversely affect our business.

Despite this, Upstart's revenue has continued to grow.

Upstart would always prefer direct traffic not just because it doesn't have to pay referral fees but there is a possibility for higher conversions with more competitive rates as per the extract below.

In addition, the limited information such loan aggregators collect from applicants does not always allow us to offer rates to applicants that we would otherwise be able to through direct applicant traffic to Upstart.com. Typically, the rates offered to borrowers who come to Upstart.com directly are lower and more competitive than those rates offered through aggregators. In the event we do not successfully optimize direct traffic, our ability to attract borrowers would be adversely affected.

However,...

In the third quarter of 2021, we modified our calculation of Conversion Rate

to remove what we believe to be fraudulent loan requests from the total number of rate inquiries received to better reflect actual borrower behavior. Using the prior methodology for calculating Conversion Rate, which did not exclude estimated fraudulent loan requests, our Conversion Rate for the three months ended September 30, 2021 would have been 13.5%. The impact of this change in calculating our Conversion Rate for prior periods is immaterial.

...is this sudden spike in fraudulent loan requests related to new traffic sources?

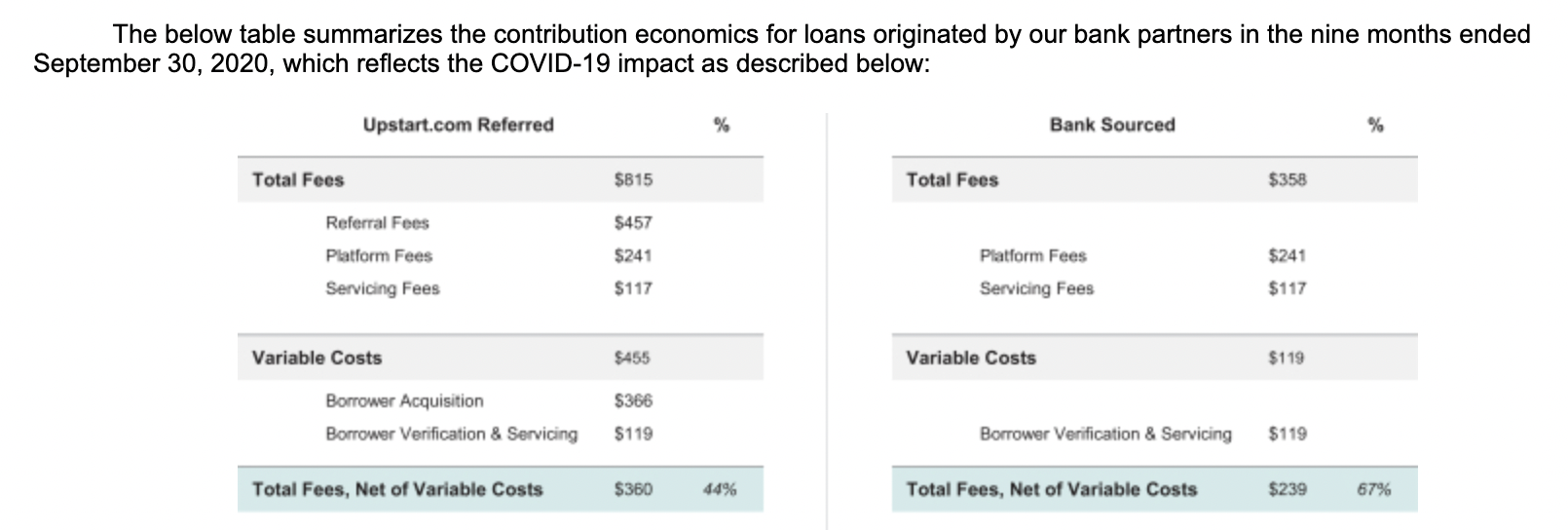

As per the table below, borrower acquisition costs has been growing slower than revenue.

As Upstart turns its focus on direct traffic, could there be a reverse in this trend leading to lower margins?

The table below is from Upstart's S-1,

The $366 (Borrow Acquisition) should be the payment to Credit Karma or for direct traffic.

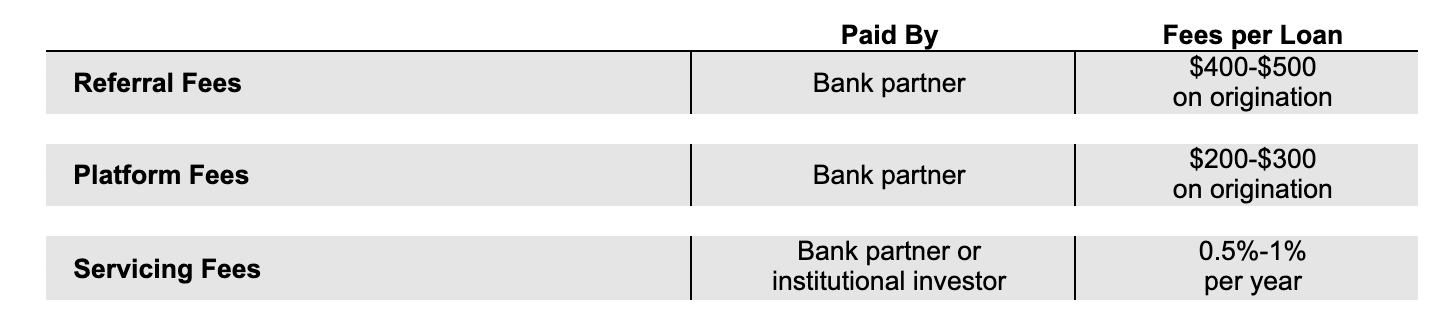

Fees are explained below.

Bank Partners

As per Upstart's 2020 Annual Report,

In addition, our bank partners have generally increasingly retained loans for their own customer base and balance sheet. In the year ended December 31, 2020, approximately 21% of Upstart-powered loans were retained by the originating bank, while about 77% of Upstart-powered loans were purchased by institutional investors through our loan funding programs. The percentage of Upstart-powered loans retained by the originating banks has fluctuated from quarter-to-quarter, but generally increased over the last few years. In general, banks can fund loans at lower rates due to the lower cost of funds available to them from their deposit base than is otherwise available in the broader institutional investment markets. Accordingly, loans retained by the originating bank generally carry lower interest rates for borrowers, which leads to better conversion rates and faster growth for our platform. Separately, as our number of bank partners grows, such banks will increasingly source new prospective borrowers from their own existing customer base and provide an incremental channel to attract borrowers. If we are unable to attract new bank partners or if we are unable to maintain or expand the number of loans held on their balance sheets, our financial performance would suffer.

Cross River Bank, or CRB, a New Jersey-chartered community bank, originates a substantial majority of the loans on our platform. In the year ended December 31, 2019 and 2020, CRB originated approximately 89% and 67%, respectively, of the loans facilitated on our platform. CRB also accounts for a large portion of our revenues. In the year ended December 31, 2019 and 2020, fees received from CRB accounted for 80% and 63%, respectively, of our total revenue. CRB funds a certain portion of these originated loans by retaining them on its own balance sheet, and sells the remainder of the loans to us, which we in turn sell to institutional investors and to our warehouse trust special purpose entities. Our most recent commercial arrangement with CRB began on January 1, 2019 and has a term of four years with an automatic renewal provision for an additional two years following the initial four year term. Either party may choose to not renew by providing the other party 120 days’ notice prior to the end of the initial term or any renewal term. In addition, even during the term of our arrangement, CRB could choose to reduce the volume of Upstart-powered loans that it chooses to fund and retain on its balance sheet or to originate at all.

This is in contrast to Affirm, who also works with Cross River Bank but has the extract below from its 2021 Annual Report.

A substantial majority of the loans facilitated through our platform are originated through our originating bank partners: Cross River Bank...

...When an originating bank partner originates a loan, it funds the loan out of its own funds and may subsequently offer and sell the loan to us. Pursuant to our agreements with these partners, we are obligated to purchase the loans facilitated through our platform that our partner offers us and our obligation is secured by cash deposits. To date, we have purchased all of the loans facilitated through our platform and originated by our originating bank partners.

That is, Cross River has been retaining loans for Upstart but not for Affirm.

Other than Cross River,

In the year ended December 31, 2020, one of our other bank partners originated approximately 24% of the loans facilitated on our platform. In the year ended December 31, 2020, the fees received from this bank partner accounted for 18% of our total revenue.

As of September 30, 2020, we had 10 bank partners, including Cross River Bank, Customers Bank, FinWise Bank, First Federal Bank of Kansas City, First National Bank of Omaha, KEMBA Financial Credit Union, TCF Bank, Apple Bank for Savings and Ridgewood Savings Bank.

As per LinkedIn, SVP of bank partnerships Michael Lock, joined in May 2020. Additionally, as per its News Releases, Upstart has continued to sign up more bank and credit union partners.

For example, First Financial Bancorp., a Cincinnati, Ohio based bank holding company. As of December 31, 2020, the Company had $16.0 billion in assets, $9.9 billion in loans, $12.2 billion in deposits and $2.3 billion in shareholders' equity.

This compares with Cross River Bank's total assets of $9.9 billion as at Nov 2020.

So while the partnership with First Financial can be material given its size relative to Cross River, Upstart did mention that...

Our sales and onboarding process with new bank partners can be long and typically takes between six to 15 months.

That said, this is still in contrast to Affirm, which comparably has less releases on new bank partnerships.

AI model benefits levelling off

According to Upstart's 2020 Annual Report below,

Further, we believe our growth over the last several years has been driven in large part by our AI models and our continued improvements to our AI models. Future incremental improvements to our AI models may not lead to the same level of growth as in past periods. In addition, we believe our growth over the last several years has been driven in part by our ability to rapidly streamline and automate the loan application and origination process on our platform. The Percentage of Loans Fully Automated on our platform was 53% in 2018 and increased to 70% in 2020. We expect the Percentage of Loans Fully Automated to level off and remain relatively constant in the long term, and to the extent we expand our loan offerings beyond unsecured personal loans, we expect that such percentage may decrease in the short term.

Is there any implication on the R&D expenditure from this given that marginal improvement is decreasing?

Credit Losses information limited

Other than the extract below from Upstart's 2020 Annual Report, there appears limited information disclosed on credit losses.

Substantially all our collection duties and obligations for loans we service that are more than 30 days past due are subcontracted to several collection agencies.

We primarily rely on three collection agencies to perform substantially all of our duties as the servicer for delinquent and defaulted loans.