Semrush vs Similarweb vs Yext - Which Stock to Buy? (November 2021 Update)

(November 2021 Update) Semrush trades at premium to Similarweb and Yext and spends less on marketing and R&D.

Semrush currently has a Market Cap to ARR at ~14x. Its ARR can be broken down into the below metrics,

A) number of customers

B) ARR per paying customer

C) revenue mix between US and non-US

The below extract from Semrush's S-1 provides some of the data points.

We estimate that, based on our current average customer spending levels, the annual global potential market opportunity for our online visibility management SaaS platform is currently $13 billion. We calculated this estimate based on the number of small and medium sized companies (those with less than 500 employees) and large companies (those with 500 or more employees) in the United States, based on information published by the U.S. Census Bureau. Approximately 94.9% of our customers are in the small and medium sized category and in such category our customers had an ARR per paying customer of $2,000 as of December 31, 2020, and our large enterprise customers had an ARR per paying customer of $4,200 as of December 31, 2020. With approximately 54% of our revenue coming from customers outside of the United States in 2020, we believe the opportunity internationally is at least as large as in the United States. We then multiplied the total number of companies in each segment by the average revenue per customer for each segment. We calculate the average revenue per customer for each segment using internal data based on actual customer spend. We assume 50% online penetration in the small company segment (those with less than 20 employees) and 100% penetration in the medium sized (those with between 20 and 499 employees) and large company segments. We believe that a 50% online penetration estimate for the small company segment is conservative as small companies are continuing to shift their operations online, particularly in response to the COVID-19 pandemic. As such, at 100% penetration, we estimate that our global annual potential market opportunity is over $20 billion, with $150 million of such annual global potential market opportunity attributable to large enterprise customers.

Using a different set of forecasts such as below,

A) number of customers grow 5x from the current 79k to 400k, or effectively market share of TAM grow from the current ~0.12% to ~0.6%;

B) ARR per paying customer increases 20% to ~$3k;

the Market Cap to ARR falls to ~2x.

In other words, if there is no de-rating from investors on the Market Cap to ARR multiple at ~14x, applying this to the increased ARR would result in a potential market cap of ~$17b.

The spreadsheet is available in our Members' section. Email [email protected] for details.

Key Operating Metrics Comparisons

Using disclosures from the investor relations section of websites of Semrush, Similarweb and Yext, we compile and compare some of their key operating metrics.

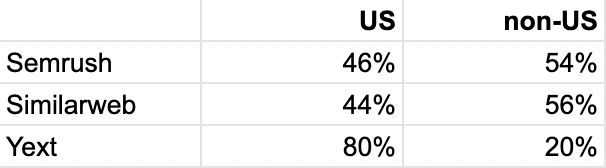

Geography mix

To begin with, both Semrush and Similarweb have just a little less than half of their businesses in the US. For Semrush specifically, about 10pp within the non-US business is in the UK. In contrast, majority of Yext is still US driven.

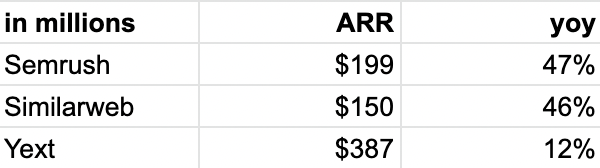

ARR

As per the Semrush's Q3'21, Similarweb's Q3'21 and Yext's Q3'22 Quarterly Earnings Releases, their respective ARR and growth are compiled below.

Semrush and Similarweb are growing at a similar level and faster than Yext. Continuing at this pace, Yext's ARR would be overtaken by Semrush in 3 years and Similarweb in 4.

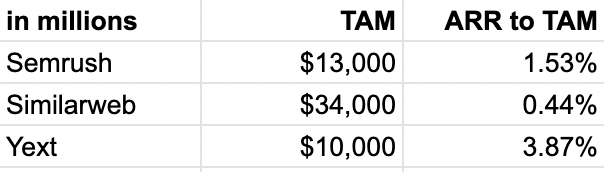

Total Addressable Market (TAM)

TAM is based on Similarweb's F-1 and Yext's S-1 extracts below.

Similarweb

We estimate that the total addressable market, or TAM, for our platform is approximately $34 billion. We calculate our market opportunity by using the total number of global companies with 100 or more employees, which we determined by referencing independent industry data from the S&P Capital IQ database. We then segment those companies in three cohorts across strategic accounts with 5,000 or more employees, enterprises with 1,000 to 5,000 employees and small and medium sized businesses with 100 to 1,000 employees. We then multiply the number of companies within each cohort by the respective average contract value per customer. The average contract value per customer is calculated by leveraging internal company data on the top two quartiles of spend per customer by employee size and customer vertical. We believe that using the top two quartiles of customer spend within each cohort represents the expansion opportunity available to us within new and existing accounts.

Yext

As a subset of digital knowledge, we estimate that there are currently over 100 million potential business locations and points of interest in the world that could benefit from our platform, representing an estimated addressable market, solely with respect to locations, of approximately $10 billion annually for our existing platform in 2017.

As per their own estimates, Similarweb has the highest TAM.

Similarweb's penetration to its TAM is also the lowest, implying higher growth potential.

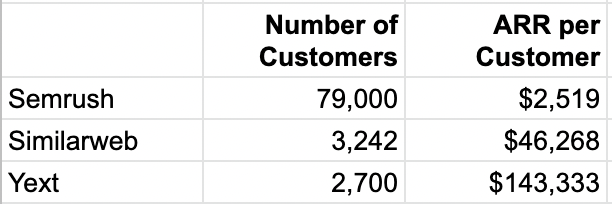

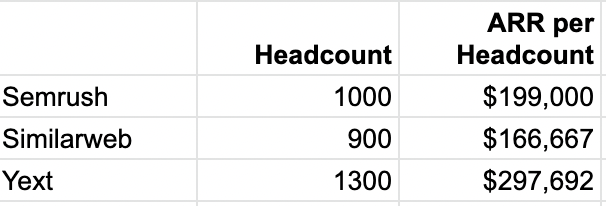

Number of Customers / ARR per Customer

Semrush has a lot more customers but a much lower ARR per customer.

Recall the Semrush's S-1 extract in the beginning of this article, 95% of Semrush's customers are SMEs with an ARR per customer of $2K.

In contrast, for Similarweb, 51% of its ARR are generated from customers that pay over $100K. Similarweb sees this customer segment as its strategic focus. Extract below from its F-1.

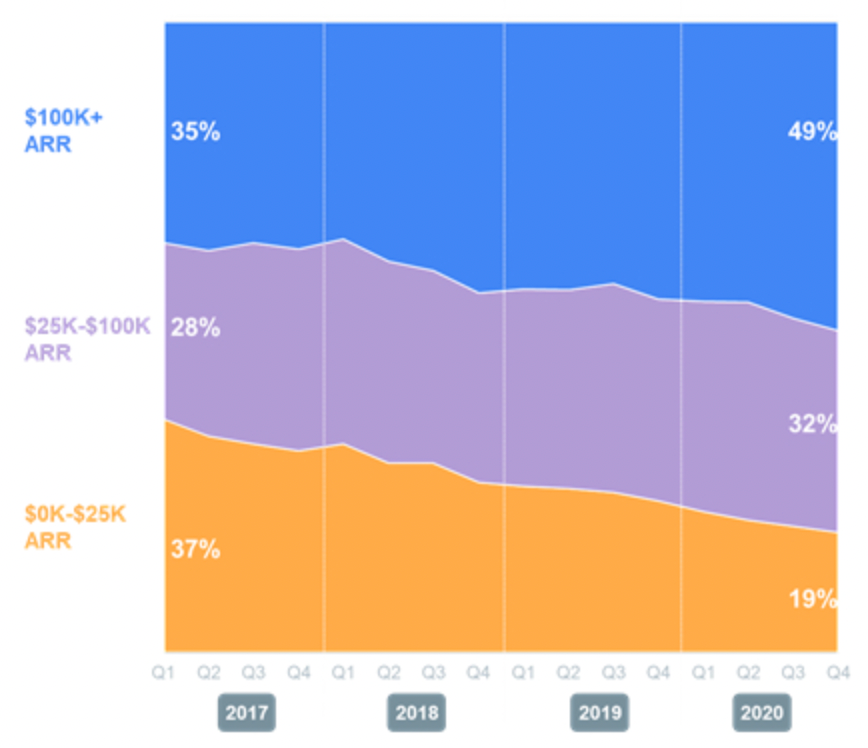

As an example, the annual recurring revenue, or ARR from our top 50 customers as of December 31, 2020 had increased by an average multiple of 12x, as compared to the ARR generated at the time of each such customer’s initial purchase.

The chart below demonstrates this trend historically.

As at Q3'21, Similarweb has 245 customers (8% of total) with ARR of $100K or more, an increase of 48% year-over-year. This is at a faster rate than number of customers growth at 27%. If this remains a pattern then the customers with ARR of $100K or more should account for a larger % of the total over time though the low level means there is still significant room for growth.

Specifically, the below extract explains Similarweb's customer acquisition strategy.

Our free offerings deliver ranking and ratings of websites and apps as of a recent date and act as an entry point for many users who often upgrade to paid subscriptions. In 2020, we attracted nearly 20 million users with these free offerings, resulting in hundreds of thousands of sales leads.

Headcount / ARR per Headcount

From a headcount efficiency perspective, Yext leads with the highest ARR per Headcount.

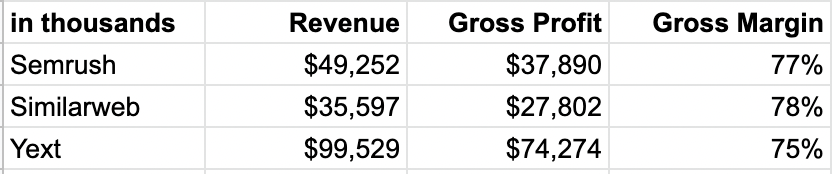

Gross Margin

The three businesses have similar gross margins...

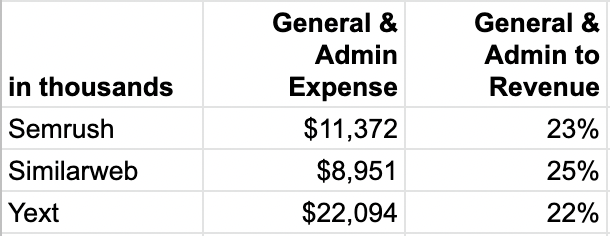

... and general admin spend.

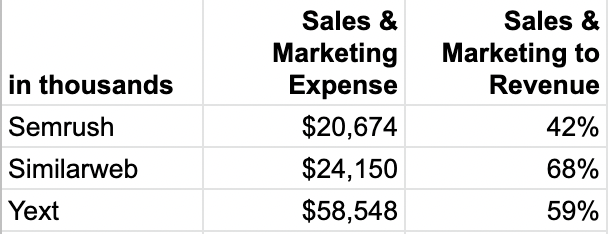

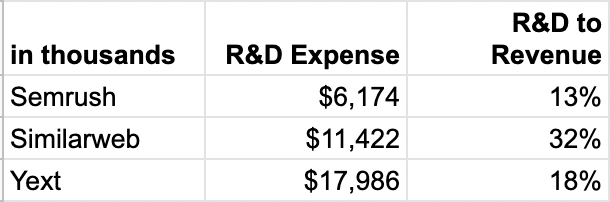

Marketing and R&D

Similarweb spends more on sales and marketing relative to revenue than both Semrush and Yext.

In terms of the absolute number though, Yext spends more than double than Semrush and Similarweb.

Similarweb also invests more in R&D relative to revenue than Semrush and Yext.

Semrush noticeably spend less in marketing and R&D in both relative and absolute terms though its growth is still relatively high. Is this because Semrush's target SME market is less competitive than enterprise? If this is so then it may not matter as much how large the TAM is as it is harder to penetrate.

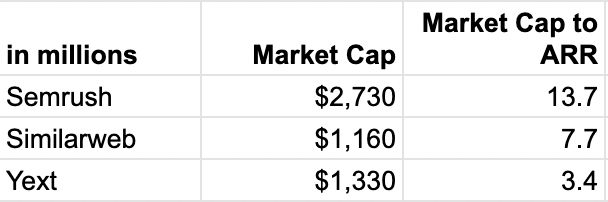

Market Cap to ARR

Semrush trades at significant premium to both Similarweb and Yext relative to their respective ARR.

Back in 2018/19, Yext's market cap was more than double its current level. The revenue for 2018 was $228m or 60% its current level. So Yext once traded at near Semrush's multiple but has since derated.